In recent years, under the influence of a series of international and domestic emergencies, Turkey's steel industry is facing multiple challenges - in February 2022, after the outbreak of the Russian-Ukrainian conflict, Turkey's steel industry is facing many challenges; In February 2023, a strong earthquake in Turkey made the steel industry worse; In October of the same year, the situation between Israel and Kazakhstan was once rigid, which further frustrated Turkish steel exports. So far this year, a series of issues such as earthquake disasters, geopolitical situations, high costs, inflation, and exchange rate fluctuations have formed the key words for the development of Turkey's steel industry, which runs through the country's 2023 steel industry market environment operation process.

According to the Turkish Steel Production Association, Turkey's steel production is currently divided into four major producing areas: Marmara producing area (production capacity: 14.7 million tons), Izmir producing area (Aegean producing area, production capacity: 11.3 million tons), Iskenderun producing area (Mediterranean producing area, production capacity: 16.7 million tons), Black Sea producing area (production capacity: 8.4 million tons).

Turkey's short-process steel mills are among the most flexible in the world, mainly using electric furnaces with scrap as raw material, so the production of local steel mills can flexibly adapt to rapidly changing market demand in order to maintain a balance between supply and demand. Smelting raw materials mainly utilize scrap steel from Europe and North America, resulting in Turkish steel mills are very sensitive to raw material price fluctuations and emphasize flexibility in production.Cutting rule and Ring forgings In addition, the unique geographical location and modern port facilities provide great convenience for the import of raw materials for steel production in Turkey and the export of finished materials, but in recent years, while enhancing international influence, the situation between Russia and Ukraine, the situation between Israel and Kazakhstan and other geographical issues have also caused a certain degree of impact on Turkey's steel import and export.

Throughout the year, the situation in Gaza led to the stagnation of Israel's demand for Turkish long materials, the triple pressure of high raw material costs, weak demand for finished materials and fierce competition from steel mills, and the situation of weak supply and demand under the internal diplomatic trap.CNC parts also affected.

So far this year, scrap import prices continue to rise, despite the weak demand for finished materials, but more optimistic market sentiment to a certain extent to support the rise in rebar prices, resulting in scrap import prices and rebar export prices almost rise and fall, the screw waste difference stabilized at 190-210 US dollars/ton, compared with the average difference of 300 US dollars/ton in previous years has narrowed. The price of scrap HMS 1/2 (80:20) imported from Turkey has dropped to as low as $350 / ton CFR this year. Therefore, it can be concluded that the export price of rebar from Turkish steel mills is at least 550 US dollars/ton FOB, which is much higher than other suppliers in the Middle East and North Africa region, and does not have a price advantage in the international market.

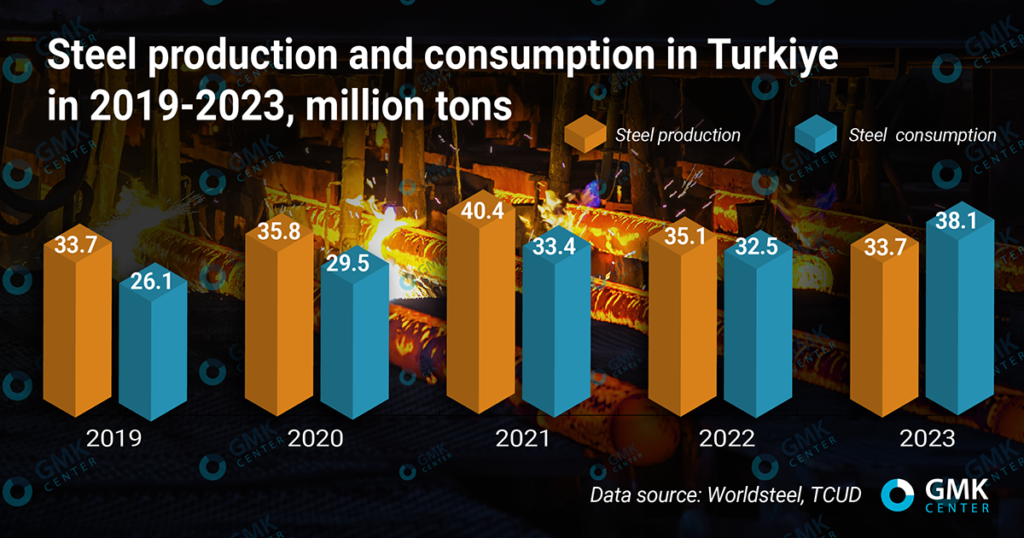

From the perspective of consumption structure, Turkey's domestic economic conditions, the construction industry and the manufacturing industry jointly determine the direction of steel demand. In 2017-2019, the continued downturn in the construction industry became the main drag on Turkey's steel consumption, which fell from 35.9 million tons in 2017 (the highest in the previous year) to 26 million tons, a decline of 27.6%. In 2020-2021, Turkey's manufacturing industry has rebounded rapidly, and at the same time, steel production capacity has also increased year by year, which has led to the recovery of steel consumption. According to the Turkish Steel Producers Association statistics, in 2021, Turkey's steel consumption increased rapidly to 33.4 million tons, an increase of 13.6%, but still less than the highest level in history.

However, entering 2022, the Russian-Ukrainian conflict has led to a sharp rise in Steel Strip For Hardware Tools, and the cost of smelting in Turkey has risen, while high inflation and the depreciation of the lira have dragged down Turkey's domestic economy, the main steel industry demand is insufficient, making Turkey's steel consumption has declined sharply, and the country's steel industry is also facing great challenges. Since the impact of the earthquake at the beginning of 2023, a series of post-disaster reconstruction projects have benefited the long material market demand. In addition, under the leadership of major steel mills, the Turkish authorities launched anti-dumping investigations on some exported varieties of steel from four Asian countries, maintaining the original anti-dumping duties unchanged, which will minimize the impact on the industry. Mysteel estimates that total steel consumption rose 18.5 per cent year-to-date to 28.9m tonnes